Medicare Glossary & FAQs

Straightforward Answers to the Most Common Medicare Questions

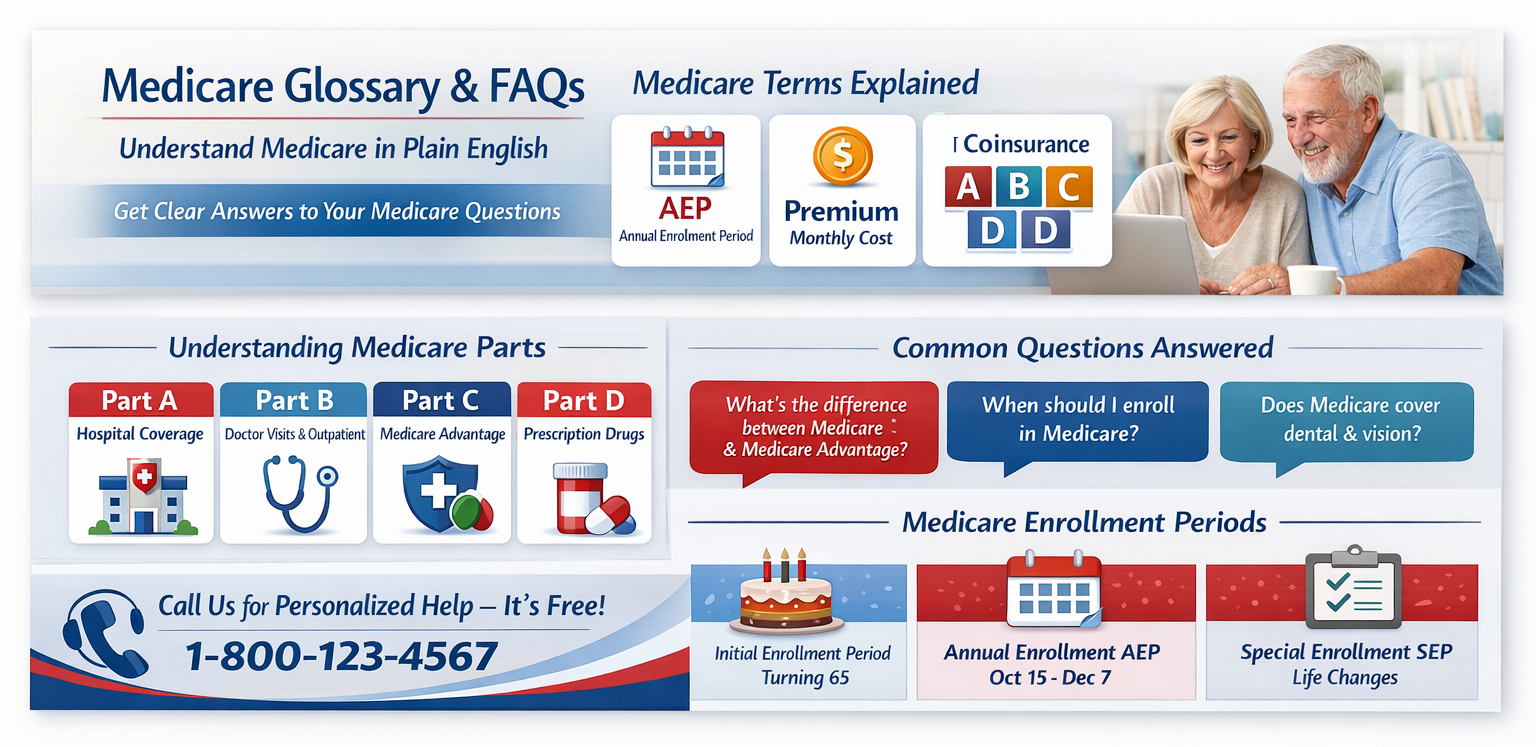

Medicare can feel like a new language — but we’re here to make it simple. Below, we have a Medicare Glossary & faqs that you’ll find clear definitions and answers to the most common questions we hear from clients.

If you don’t see your question here, just call (888) 341-2229 or schedule a free consultation — we’ll be happy to help.

Medicare Glossary

Annual Enrollment Period (AEP)

The time each year — October 15 to December 7 — when you can review, change, or enroll in a Medicare Advantage or Prescription Drug Plan.

Coinsurance

The percentage you pay for covered services after meeting your deductible.

Copayment (Copay)

A fixed amount you pay for a covered healthcare service, such as a doctor visit or prescription.

Deductible

The amount you pay out-of-pocket for healthcare services before your plan begins to pay.

Formulary

The list of prescription drugs covered by your Medicare plan.

Medicare Advantage (Part C)

A private plan that combines Parts A and B — and often includes Part D, dental, vision, and hearing benefits — all in one.

Medicare Part A

Covers hospital care, skilled nursing, hospice, and some home health services.

Medicare Part B

Covers doctor visits, outpatient care, preventive services, and medical equipment.

Medicare Part D

Provides prescription drug coverage, available as a standalone plan or through most Medicare Advantage plans.

Medigap (Medicare Supplement)

A private insurance policy that helps pay some of the costs Original Medicare doesn’t cover, such as copays, coinsurance, and deductibles.

Network

The group of doctors, hospitals, and healthcare providers that contract with a specific Medicare Advantage plan.

Open Enrollment for Medicare Advantage (OEP):

Every year from January 1 – March 31. If you’re already in an Advantage plan, you can make a one-time switch.

Out-of-Pocket Maximum

The maximum amount you’ll pay for covered services in a plan year. After you reach this amount, your plan pays 100% of covered costs.

Premium

The amount you pay each month to keep your coverage active.

Special Enrollment Period (SEP)

A time outside the regular enrollment periods when you can make changes to your coverage due to certain life events, like moving or losing other insurance.

Frequently Asked Questions

1. What is the difference between Medicare and Medicare Advantage?

Medicare (Parts A and B) is run by the federal government and covers hospital and medical services. Medicare Advantage (Part C) is offered by private insurers and includes all Original Medicare benefits plus extras like dental, vision, hearing, and prescription drug coverage — often for little or no additional premium.

2. When should I enroll in Medicare?

Most people enroll during their Initial Enrollment Period, which begins three months before your 65th birthday and ends three months after. If you’re still working or have other coverage, there may be different rules — we can help you figure out what applies to you.

3. Do I have to pay for Medicare?

Many people don’t pay a premium for Part A, but Part B usually has a monthly cost. Medicare Advantage and Prescription Drug plans may also have their own premiums, copays, or deductibles.

4. Can I change my plan later?

Yes! Each year during the Annual Enrollment Period (October 15 – December 7), you can review your coverage and switch if you find a better plan. Some life events may also qualify you for a Special Enrollment Period.

5. Does Medicare cover dental, vision, or hearing?

Original Medicare does not. However, many Medicare Advantage plans include these benefits — and some even offer allowances for glasses, hearing aids, or dental care.

6. What happens if I don’t sign up when I’m first eligible?

If you miss your initial enrollment period and don’t have other qualifying coverage, you could face late enrollment penalties for Part B or Part D. We’ll help you avoid those costly mistakes by reviewing your timeline and options early.

7. How much does your help cost?

Nothing at all. Our services are completely free — there’s no cost or obligation to you. We’re compensated directly by the insurance carriers, so our only focus is helping you find the right plan.

8. Why should I work with a Medicare specialist?

Because the right plan depends on your doctors, medications, and lifestyle. Our licensed team compares multiple carriers and plans to find the one that fits you. We make the process easy, accurate, and personal — with the confidence that comes from over 30 years of experience.

9. Which Providers does the Medicare Advantage Specialist Group LLC use?

We partner with a variety of leading Medicare Advantage providers to ensure you receive the benefits you truly deserve. These include: Aetna, Blue Cross, Humana, People’s Health, UnitedHealthcare, and Wellcare.

This broad selection allows us to compare options objectively and recommend the plan that best matches your health needs, doctors, prescriptions, and budget.